Navigating the Bill of Materials Strain From Surging Semiconductor Memory Manufacturing Costs

Smartphone production is facing an intense hardware budget squeeze. Surging mobile RAM and storage costs are forcing brands to recalculate retail pricing strategies.

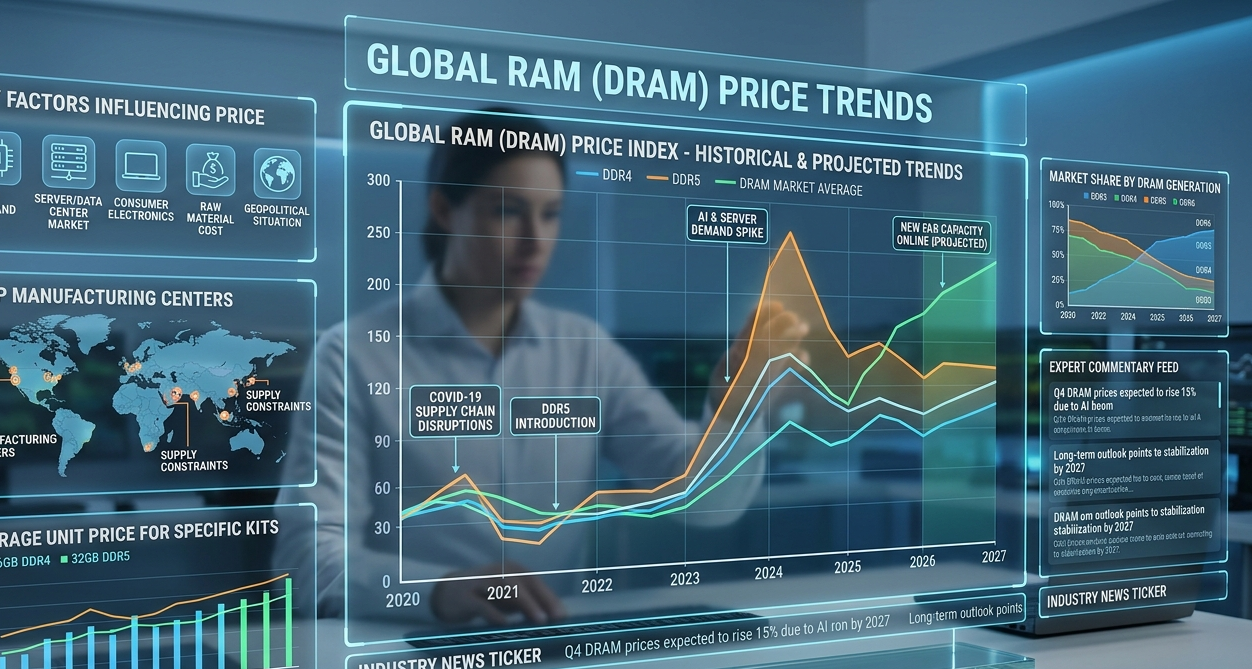

The underlying financial reality of manufacturing premium mobile devices has shifted dramatically due to intense price volatility within the semiconductor supply chain. Market analysis from industry research groups like TrendForce reveals an unprecedented spike in contract pricing for vital memory components, specifically mobile LPDDR5X RAM and high-capacity UFS flash storage layers.

Historically, the memory subsystem accounted for a predictable 10% to 15% share of a flagship smartphone's total Bill of Materials (BOM). Due to systemic supply constraints and complex wafer manufacturing yields at advanced fabrication foundries, that cost baseline has expanded significantly, now consuming up to 30% or 40% of the hardware budget on mainstream mid-tier and flagship devices.

Faced with an extra financial burden on every single unit produced, smartphone brands are dividing into distinct strategic paths. Premium market leaders can typically absorb these component cost increases or adjust retail pricing due to higher consumer price tolerance. Conversely, brands operating in thin-margin, entry-level tiers are forced to re-evaluate their hardware lineups—either by scaling back baseline configurations to smaller memory capacities or modifying launch schedules to manage elevated chip pricing.